Saving is always wise — but is a savings account the best way to save money?

What is a Savings Account?

While checking accounts are used to store money for daily expenses like food or bills, savings accounts are used to store money over a long period of time. Although fees and withdrawal limits may be drawbacks, savings accounts also offer safety and reliability.

Each type of savings account differs in interest and accessibility, but they generally share these pros and cons:

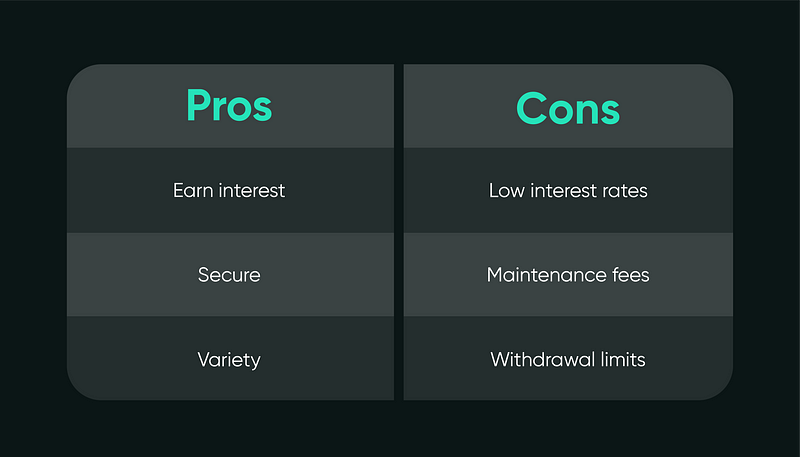

Pros

Earn Interest

The biggest advantage to savings accounts is that they build interest over time. With your money deposited in their accounts, banks are able to loan money to other customers. Banks return the favor to you by paying interest on the savings accounts. Therefore, the longer you keep the money in your savings account, the more money and the more worthwhile it will be for you. Typically, it’s advised to not touch your savings account as long as possible. Forget about it for some years, don’t do anything, and you’ll earn money.

Secure

If you choose a savings account from a Federal Deposit Insurance Corporation (FDIC) member bank, your account will be insured up to $250,000 under the law. With federal protections, savings accounts are a reliable way to store your emergency funds. To find out if your bank is FDIC-insured, check out FDIC’s Bank Data Guide.

Different Kinds for Different Needs

Besides standard savings accounts, banks are offering more varieties of ways to help you save. High-yield accounts offer higher APY rates compared to basic accounts. The only catch is that you may not be able to access them at bank branches or an ATM. Banks also are offering different types of savings accounts depending on customers’ niche needs. The 529 Plan is tailored for saving for college education costs, offering tax benefits depending on the state you open one in. These specialty accounts all offer interest and security, although they may have stricter restrictions on withdrawals and spending.

Cons

Slow and Low Interest Rates

As much as the idea of earning money while doing nothing sounds attractive, the interest rates are incredibly low. The current national average interest rate according to the FDIC is 0.05% APY. Compared to interest rates of other deposit account options like Certificate of Deposits (CDs) and money market accounts, 0.05% is a very low number. For a full view on national rates on the different kinds of accounts, check out FDIC’s Weekly National Rates and Rate Caps charts.

Fees

To maintain services, banks may ask for a monthly maintenance fee of $4 or $5. In addition, if your funds fall below a minimum requirement, you will be asked to pay fees as well. If you do choose to open a savings account, it is crucial to keep yourself updated on any updated terms and conditions to make sure you avoid fees that may deduct from your earned interest.

Withdrawal Limits

Under the Federal Reserve’s Regulation D, savings account holders are not able to withdraw or transfer funds from their accounts more than six times in a month. This limit allows banks to still reserve some of your deposit and stay in business by using the rest of your money for other services. If you exceed the limit, you may be charged fees, or the Fed may close your account altogether.

However with the widespread impact of the pandemic on individual finances, the Fed lifted the limit on the number of withdrawals and transfers on April 24 to help account holders access their savings and emergency funds.

Main Takeaways

Before opening a savings account, set your personal goals and consider which of the pros and cons matter more to you. There are different kinds of savings accounts, but there are also alternatives to long-term saving rather than opening a basic savings account. You may also look into different kinds of savings accounts and open multiple ones.